In this round up, we cover the key issues and announcements for February 2022 and what a month!

The ATO has launched an attack on trust and trust distributions via the section 100A integrity rules. Plus, a related draft determination updates the guidance on Division 7A and UPEs.

And, two important decisions have been handed down in employer v contractor High Court cases. There is a little misinformation circulating in the profession because of the court’s emphasis on the terms of the contracts in these cases, but it is never that simple and it will be important for practitioners to understand the nuances.

As always, we’re here if you there are any questions you have so please contact John Kalachian or Henry Zhao!

From Government

Deductibility of COVID-19 test expenses

The Government has announced that legislation will be introduced to ensure that work‑related COVID‑19 test expenses incurred by individuals will be tax deductible. Changes will also be made to ensure that FBT will not be payable by employers if they provide fringe benefits relating to COVID‑19 testing to their employees for work‑related purposes.

The changes for deductions will be effective from 1 July 2021, with the FBT changes to apply from 1 April 2021.

Having said that, it is important to note that the ATO will be reviewing claims to determine if they are reasonable. For example, an individual who makes a large deduction claim for COVID-19 test expenses could come under scrutiny if they have been primarily working from home during the income year.

More information – Media release – Tax deductibility of COVID-19 test expenses

NSW COVID-19 support package

The NSW Government has introduced a new small business support package which provides eligible employing businesses with a lump sum payment of 20% of weekly payroll, up to a maximum of $5,000 per week for the month of February 2022. The minimum weekly payment for employers is $750 per week. Eligible non-employing businesses will receive $500 per week (paid as a lump sum of $2,000).

In order to access the package, businesses must have:

- An aggregated annual turnover between $75,000 and $50 million (inclusive) for the year ended 30 June 2021; and

- Experienced a decline in turnover of at least 40% due to Public Health Orders or the impact of COVID-19 during the month of January 2022 compared to January 2021 or January 2020; and

- Experienced a decline in turnover of 40% or more from 1 to 14 February 2022 compared to the same fortnight in either 2021 or 2020 (you must use the same comparison year utilised in the decline in turnover test for January); and

- Maintained their employee headcount from 30 January 2022.

The support package only covers the month of February 2022. Applications for support can be made through Service NSW by using a My Service NSW account (see the link below).

More information

From the ATO

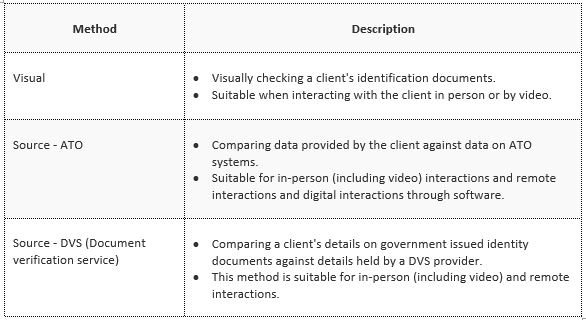

Verifying client identity

The ATO has released detailed guidelines to be followed by tax practitioners in establishing and confirming the identity of their clients, as part of meeting requirements prescribed by the TPB with respect to minimising tax and identity fraud. The guidance is not yet mandatory but both the ATO and the TPB are indicating that this is a possibility in the future.

ID checks should be carried out for certain individuals including:

- All new clients, including representatives of new clients

- New representatives of existing clients

- Existing clients where you have concerns the client may not be who they say they are.

For the final category the ATO also provides a list of high-risk transactions or requests where it would be important to confirm the person’s ID, particularly where they are dismissive or recalcitrant in providing information. These can include:

- Requests for bank account changes

- Requests to amend tax returns or statements (particularly to increase refunds)

- Requests to lodge returns or statements with significant or unusual refunds

- Requests to release or roll-over super

- Requests for information from ATO systems including pre-fill information

- Requests for personal information that would ordinarily be known to individuals or entities

- Where a person is acting on behalf of another person or multiple persons.

The verification process involves verifying two separate proof of identity documents using one or a combination of the methods outlined below. The exception is when a primary photographic proof of identity document can be verified using the visual method (e.g. a client directly showing you the document).

For representatives of clients you must verify both:

- The representative’s identity using the methods described above (the Source – ATO method cannot be used for this purpose); and

- That the representative is authorised through relationship verification.

More information – Strengthening client verification guidelines

The 85% lodgement target

In light of many tax practitioners struggling to reach the 85% on-time lodgement target due to the additional work and disruptions flowing from the COVID-19 pandemic, the ATO has provided some guidance on practical steps that can be taken to track your progress and minimise issues.

The first point is that you can monitor your on-time lodgement performance for income tax returns online through Online services for agents. This will allow you to track the status of your client’s returns and be aware of any lodgements outside the ‘normal’ periods – e.g., returns that need to be lodged earlier than usual.

Another important point is that updating your client list regularly will help ensure that former clients who no longer use your services are not included in your lodgement program performance calculation.

If you are engaged by new clients (or are re-engaged by former clients) with overdue prior year income tax returns, the on-time lodgement performance will only be affected if you lodge the current year’s return after the due date or deferred due date.

All clients attached to your registered agent number with an expected lodgement will be included in your on-time lodgement performance calculation. If a client is not required to lodge a tax return or FBT return, then this should be advised to the ATO as soon as possible.

More information – What you can do to meet the performance requirement

Rulings, determinations & guides

Section 100A reimbursement agreements

Section 100A is an anti-avoidance provision contained in the Income Tax Assessment Act 1936 that is broadly aimed at situations where the economic benefit of trust distributions (e.g., the actual funds) is directed to an entity who is not presently entitled to the income (and assessed on the amount). This can include situations where a trustee appoints income to a particular beneficiary but the funds representing the entitlement are provided to another individual or entity. When section 100A applies the trustee is generally taxed on the income at penalty rates rather than the presently entitled beneficiary being assessed.

The ATO has released a draft ruling which sets out the ATO’s concerns in this area and explains situations where section 100A is likely to apply.

There are some exceptions to section 100A, including where the income has been appointed to a beneficiary who is under a legal disability (e.g., minor beneficiaries). The other major exception relates to transactions that are in the ordinary course of a family or commercial dealing. The ATO looks at this exception in detail in the draft ruling and indicates that the exception won’t necessarily apply just because a particular strategy is common or involves family members. For example, the ATO suggests that section 100A could apply to some situations where a dependent child gifts money that is attributable to a family trust distribution to their parents.

Many practitioners and clients will be surprised by the approach taken by the ATO in relation to section 100A and many family groups will end up paying more tax on income generated by family trusts in coming years as a result of the ATO’s guidance in this area. It is vital for practitioners to understand the ATO’s concerns and the type of tax planning strategies that carry a reasonably high level of risk.

In connection with the draft ruling on section 100A the ATO has also released a practical compliance guideline which explains how the ATO will apply its compliance resources to trust distribution arrangements. The PCG sets helps to explain the level of risk associated with a range of situations.

The PCG provides detailed examples of arrangements falling within different risk zones (from white to red). For example, the ATO suggests that when a trust appoints income to an individual, but the funds are paid into a joint bank account that the individual holds with their spouse then this would ordinarily be a low-risk scenario and the ATO is unlikely to apply compliance resources to this type of arrangement.

On the other hand, the ATO indicates that where an individual adult beneficiary is made presently entitled to trust income the presence of any of the following features would likely cause the arrangement to fall within the high-risk category:

- Funds that represent the entitlement are paid to the parent of the beneficiary in connection with expenses incurred by the parent before the beneficiary turned 18 years of age;

- The trustee applies the funds that represent the entitlement against a debit balance account for the beneficiary (for example, an amount recorded in the trust’s accounts as a loan) representing expenses incurred by the trustee in respect of the beneficiary before they turned 18 years of age.

- Funds that represent the entitlement are made available to the parent of the beneficiary by way of loan or gift; or

- The beneficiary is a non-resident and the funds that represent the entitlement are made available to another party by way of loan or gift.

The ATO has also released a taxpayer alert in this area, TA 2022/1, which warns taxpayers that the ATO will be reviewing trust arrangements where parents enjoy the economic benefit of trust income appointed to their children who are 18 years of age or older. This is clearly an area of ATO focus at the moment and practitioners and clients need to take the time and effort to understand the ATO’s concerns and steps that can be taken to reduce the risk of section 100A applying.

Updated guidance on UPEs and Division 7A

This draft determination provides some updated guidance on the time at which the ATO consider amounts owed by trusts to corporate beneficiaries could be considered loans for Division 7A purposes. The draft TD looks at when an unpaid present entitlement (UPE) will start being treated as a loan for Division 7A purposes and when the ATO will take the view that a loan exists even if a sub-trust arrangement is in place.

Since late 2009 the ATO has taken the view that UPEs owed by trusts to related companies can be treated as loans for Division 7A purposes. In previous guidance the ATO has indicated that the UPE will start being treated as a loan at some point during the income year after the year in which the income was appointed to the corporate beneficiary. However, the new draft TD potentially changes this in some cases.

The ATO now states that if a trustee resolves to appoint income to a private company beneficiary then the time the UPE starts being treated as a loan will depend on how the entitlement is expressed by the trustee (e.g., in trust distribution resolutions etc):

- If the company is entitled to a fixed amount of trust income (e.g., a specific dollar amount), the UPE will generally be treated as a loan for Division 7A purposes in the year the present entitlement arises; or

- If the company is entitled to a percentage of trust income, or some other part of trust income identified in a calculable manner, the UPE will generally be treated as a loan from the time the trust income (or the amount the company is entitled to) is calculated, which will often be after the end of the year in which the entitlement arose.

When it comes to sub-trust arrangements, the ATO indicates that where the trustee sets aside an amount from the main trust and holds it on sub-trust for the exclusive benefit of the company, the present entitlement to income is paid and there is no UPE. In that case, the company has a new right to call for payment of the sub-trust funds.

If the company chooses not to exercise that right then this does not constitute financial accommodation in favour of the trustee. However, the ATO’s view is that the company would be providing financial accommodation (i.e. a loan for Division 7A purposes) if the company allows those funds to be used by a shareholder or their associate, regardless of whether the arrangement is on commercial terms.

The TD represents a significant departure from the ATO’s previous guidance in this area, although the ATO indicates that the new approach will only apply to trust entitlements arising on or after 1 July 2022.

Commercial debt forgiveness: the natural love and affection exclusion

The ATO has clarified that the natural love and affection exclusion from the commercial debt forgiveness rules can only apply where the creditor is an individual. This means that companies or other trusts cannot generally rely on the exclusion, although the ATO does note that this could potentially include an individual in their capacity as a trustee of a trust or as a partner in a partnership.

The ATO indicates that the legislation in this area requires a direct connection between the forgiveness and the natural love and affection, and that the natural love and affection must arise in consequence of ordinary human interaction. For this to occur, the creditor must be a natural person (individual) and the object of their love and affection must be one or more other natural persons (another individual)

However, the ATO indicates that the debtor doesn’t necessarily need to be a natural person. That is, an individual can forgive a debt owing by a company or trust if the forgiveness has a direct connection with natural love and affection for an individual associated with that entity (e.g., where a parent forgives a debt owed by a company that is 100% owned by their child).

Deductibility of expenses relating to establishing employee share schemes

The draft determination indicates that the expenses incurred in establishing or amending the terms of an employee share scheme (ESS) are not deductible to the employer company under section 8-1 because they are capital in nature. If the employer company is carrying on a business, these expenses should generally be deductible to the employer company over five years under the blackhole expenditure rules in section 40-880.

The types of expenses that would typically be covered by the determination include:

- Legal fees incurred in establishing an employee share trust or the ESS plan rules;

- Start-up costs such as trustee company commencement charges for employee share trusts; and

- Registration fees with various authorities such as stamp duty and ASIC fees.

On the other hand, the ATO indicates that ongoing expenses associated with the administration of an ESS can be deductible under section 8-1. Ongoing expenses may include brokerage fees, audit fees, bank charges, making new offers to employees under an existing ESS and other ongoing administrative expenses.

Cases

The employee vs contractor distinction

- Construction, Forestry, Maritime, Mining and Energy Union v Personnel Contracting Pty Ltd [2022] HCA 1

- ZG Operations Australia Pty Ltd v Jamsek [2022] HCA 2

The employee / contractor distinction continues to be a difficult area for many businesses and workers, and we continue to see disputes arising in this area. In February 2022 the High Court handed down decisions in two cases which looked at whether workers were employees or contractors of the relevant businesses.

In Personnel Contracting, an individual was offered a role with a labour hire company and signed an Administrative Services Agreement (“ASA”) which described the individual as a “self-employed contractor”. The company assigned the individual to work on two construction sites run by a client of the company. The individual performed basic labouring tasks under the supervision and direction of supervisors employed by the client.

The individual and the CFMMEU commenced proceedings against the labour hire company in the Federal Court, arguing that he was an employee under the Fair Work Act 2009. The primary judge held that the individual was an independent contractor and an appeal to the Full Federal Court was dismissed. Both courts applied a multifactorial approach, referring to the terms of the ASA and the work practices imposed by the company and its client.

However, the High Court held that the individual was an employee of the company. The majority held that where parties have comprehensively committed the terms of their relationship to a written contract and this is not challenged on the basis that it is a sham etc, the characterisation of the relationship is to be determined with reference to the rights and obligations of the parties under that contract. Absent a suggestion that the contract has been varied, or that there has been conduct giving rise to an estoppel or waiver, a wide-ranging review of the parties’ subsequent conduct is not necessary or appropriate.

Under the ASA, the company had the right to determine for whom the individual would work, and the individual promised the company that he would co-operate in all respects in the supply of his labour to the client. In return, the individual was entitled to be paid by the company for the work he performed.

This right of control, and the ability to supply a compliant workforce, was the key asset of the company’s business as a labour-hire agency. These rights and obligations constituted a relationship between the company and the individual of employer and employee.

The emphasis on the terms of the contract was repeated in ZG Operations. That case involved two individuals engaged as truck drivers by a business run by a company over an extended period of time. The individuals were initially engaged as employees of the company and drove the company’s trucks. However, in the mid-1980’s the company offered the individuals the opportunity to become contractors and purchase their own trucks. The individuals agreed to this and set up partnerships with their respective wives.

Each partnership executed a written contract with the company for the provision of delivery services, purchased trucks from the company, paid the maintenance and operational costs of those trucks, invoiced the company for its delivery services, and was paid by the company for those services. The income from the work was declared as partnership income for tax purposes and split between each individual and their wife.

The High Court has now held that the individuals were not employees of the company. Consistent with the decision in the Personnel Contracting case (above), a majority of the Court held that where parties have comprehensively committed the terms of their relationship to a written contract (and this is not challenged on the basis that it is a sham or is otherwise ineffective under general law or statute), the characterisation of the relationship must be determined with reference to the rights and obligations of the parties under that contract.

After 1985 or 1986, the contracting parties were the partnerships and the company. The contracts between the partnerships and the company involved the provision by the partnerships of both the use of the trucks owned by the partnerships and the services of a driver to drive those trucks. This relationship was not a relationship of employment.

These cases show how important it is to consider all relevant facts in deciding whether a worker should be classified as an employee or contractor. Leaving this basic distinction aside, practitioners and clients also need to be mindful of the fact that even if a worker is not an employee under general principles they could still be classified as a deemed employee for certain purposes, such as under the SG rules.

Directed payments for services

Mobbs v FC of T [2022] AATA 201

This case looked at whether certain payments and shares should be included in the assessable income of an individual or their company.

The individual had provided services to several businesses as an executive (e.g. CEO, executive chairman or director) and was arguing that the payments and shares issued in relation to the services should be included in the company’s income on the basis that he was not personally engaged as a director of the other businesses, but was operating through his own company as a contractor. The ATO argued that the individual was in fact deriving the payments and shares in his personal capacity and then subsequently directing the payments etc. be made to the company, in which case he should be assessed personally.

This is a relatively common scenario and the courts have previously found in favour of the ATO’s view in some cases, particularly in situations involving directorships because only an individual can be appointed as a director of a company. The issue for many taxpayers, including the individual in this case, is that often there is no documentary evidence directly corroborating that the business / employer has engaged the company rather than the individual in relation to the services.

In this case the AAT agreed with the Commissioner and found that the amounts should be included in the assessable income of the individual. A lack of documentary evidence meant that the individual found it difficult to support the basis they had taken.

The AAT noted that the taxpayer’s significant experience in managing businesses should have led them to take greater care to ensure that their asserted position was clearly documented. That is, the AAT suggested that it might have been possible for the amounts to have been assessable to the company had the arrangement been structured in a more formal manner. Once again, we see an example of where a taxpayer’s argument fails (at least in part) due to a lack of evidence and formal documentation.

Legislation

Superannuation reforms and extension of temporary full expensing

This Bill, containing a number of significant changes, has passed through Parliament and has received Royal Assent.

Temporary full expensing extended

The Bill extends the temporary full expensing regime by 12 months to 30 June 2023. This means that a range of business entities will be able to claim a full deduction for the cost of depreciating assets regardless of their cost. The rules were due to expire on 30 June 2022. For companies it is important to note that the loss carry back rules have not yet been extended to 30 June 2023, we are still waiting on the relevant legislation to be passed.

Superannuation reforms

The Bill legislates a series of reforms that will take effect from 1 July 2022 including:

- Work test – Repeal of the work test for non-concessional and salary sacrificed contributions made by individuals aged between 67 and 75

- Expanding access to bring forward rule to those aged 67-75 – Enabling individuals aged between 67 and 75 to make non-concessional superannuation contributions under the bring-forward rule

- Abolition of $450 SG threshold – removing the $450 per month income threshold under which employees do not have to be paid the superannuation guarantee by their employer

The Bill also contains a number of other reforms including:

- First home saver scheme – increasing the maximum amount of voluntary contributions that could be released under the First Home Super Saver Scheme (FHSSS) from $30,000 to $50,000 (applying to requests on or after 1 July 2022).

- Reducing eligibility age for downsizer contributions – reducing the eligibility age for making downsizer contributions into superannuation from 65 to 60 years of age from 1 July 2022 (i.e., from 1 July 2022, those aged 60 years of age or more at the time a downsizer contribution if other eligibility criteria met).

- ECPI calculation – allows trustees to use their preferred method of calculating exempt current pension income where the fund is fully in the retirement phase for part of the income year but not for the entire income year (applies from the 2021-22 income year onwards).

See also the media statements from Senator Jane Hume, Parliament passes legislation to enhance the superannuation system and the Treasurer, Josh Frydenberg, Parliament passes legislation to drive investment and support first home buyers.