Do You Know About Allocation of Professional Firm Profits?

The Australian Tax Office (ATO) has a new rule. They’re going to be talking to some professional workers, like lawyers or engineers (these are called Individual Professional Practitioners or IPP’s), to see how they are treating profits in their respective firms.

The Guideline, PCG 2021/4, updates old rules from 2015 and is effective from 1 July 2022. It looks at professional firm profits and how much of these are taxed in the hands of the IPP and how much is transferred or moved to another business or individual they’re connected with. Doing this can sometimes mean they pay less tax.

Before using the Guidelines, Firms need to assess two things – these are called ‘gateways’.

- They need to see if their way of handling profits makes sense for their business (this is called a ‘commercial rationale’).

- They also need to make sure their way of handling profits doesn’t include high risk arrangements.

If both of these gateways are clear, Firms can calculate their results compared to the ATO’s risk assessment scoring table

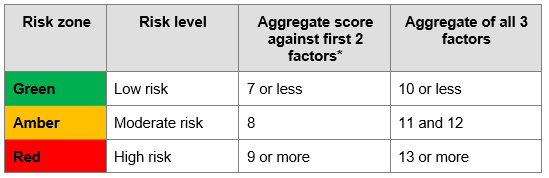

1. Complete the risk assessment scoring table.

2. Work out the risk zone

Firms are required to work out their ‘total effective tax rate’, which is a way to see how much tax they are really paying. They also need to calculate the proportion of profits returned in the hands of the IPP. If an IPP includes all their profit from their firm in their individual tax return, they are in the ‘green zone’ and don’t need to worry about the other risk rules.

If an IPP does the calculations based on the table above and the results work out in the Red or Amber zones, the ATO is likely to conduct further analysis, ask for a review of information, or cases may proceed straight to tax audit.

For profits between 1 July 2017 to 30 June 2022, Firms can still use the old rules if their way of handling profits makes sense for their business and doesn’t include high risk arrangements. These will be seen as low risk.

But if a Firm’s way of handling profits was seen as low risk with the old rules but is a higher risk with the new Guideline, they can keep using the old rules until 30 June 2024.

Remember, this is a new & complicated tax rule and the incorrect treatment can have many ramifications on your personal and business tax affairs.

As an Australian tax expert, I’m here to help you understand these changes and make sure you’re doing everything right. If you have any questions or would like to know more, then please contact us directly.